Dental implants can transform your smile, but the cost often feels overwhelming. Many people put off this important treatment because they worry about paying thousands of dollars upfront.

Most dental implant payment plans cover the entire treatment cost, including the implant post, abutment, crown, and often preliminary procedures like bone grafting or extractions, allowing you to spread payments over several months or years.

Payment plans for dental implants can work alongside your insurance to lower what you pay out of pocket.

You have more options than you might think, from interest-free periods to low monthly payments that fit your budget. Understanding what financing covers and how to qualify helps you move forward with confidence.

This guide has dental implant payment plans explained, so you can make the best choice for your smile and your budget.

Key Takeaways

- Dental implant payment plans typically cover all treatment costs from the implant post to the final crown and can be spread over months or years

- You can combine multiple payment methods, including insurance benefits, health savings accounts, third-party financing, and in-office payment plans to reduce costs

- Approval depends on factors like your credit score, income, down payment amount, and the specific financing option you choose

What Dental Implant Payment Plans Usually Cover

Most dental implant payment plans cover the complete procedure from start to finish, letting you spread the cost over several months or years. Understanding what’s included helps you compare options and avoid surprise expenses.

Components of a Dental Implant Procedure Included in Plans

Payment plans typically cover all major parts of your dental implant procedure. This includes the titanium post that goes into your jawbone, the abutment that connects the post to your replacement tooth, and the crown that serves as your permanent teeth.

Most plans also include preliminary work you might need before getting your implants. If you need a tooth extraction to remove a damaged tooth, that’s usually covered.

Bone grafting procedures are often included too, which you might need if your jawbone isn’t strong enough to support the titanium post.

Common inclusions in payment plans:

- Titanium implant posts

- Abutments and connectors

- Custom crowns or prosthetic teeth

- Tooth extractions

- Bone graft procedures

- Initial consultations and X-rays

For full mouth dental implants or all-on-4 implant systems, payment plans typically cover the entire treatment package. This means all the posts, connectors, and the full arch of permanent teeth are included in your monthly payments.

Have questions about dental implant payment plans or what your treatment may include? Contact Northwest Oral Surgeons today for clear guidance, personalized options, and transparent costs.

Common Exclusions and Limitations

Not everything related to dental implants gets covered by payment plans. Many plans exclude routine follow-up visits after your initial healing period.

You might pay separately for annual checkups or cleanings around your implants. Some financing options won’t cover complications that happen after your procedure is complete.

If you develop an infection months later or need repairs to your crown, you may face additional charges. Plans often have limits on how much they’ll finance.

If the cost of dental implants exceeds a certain amount, you might need to make a larger down payment or find additional financing.

Items typically not covered:

- Routine dental cleanings

- Post-treatment complications

- Replacement crowns after several years

- Sedation upgrades beyond basic options

- Same-day or expedited treatment fees

Typical Payment Periods and Structures

Dental implant financing offers flexible payment periods ranging from a few months to several years. Short-term plans usually run 6 to 24 months, while longer arrangements can extend up to 5 or 7 years depending on your dental implant costs.

Interest-free periods are common with many payment plans. You might get 6, 12, or even 24 months to pay off your balance without any interest charges.

After this promotional period ends, standard interest rates apply to any remaining balance. Monthly payment amounts depend on the total cost of dental implants and your chosen timeframe.

A $3,000 single implant might cost you $125 per month over 24 months with no interest. Or around $60 per month if you extend payments to 60 months with interest included.

Exploring Dental Implant Financing Options

You have several ways to pay for dental implants over time, including plans directly through your dentist’s office, loans from banks or credit unions, and special healthcare credit cards that work specifically for medical expenses.

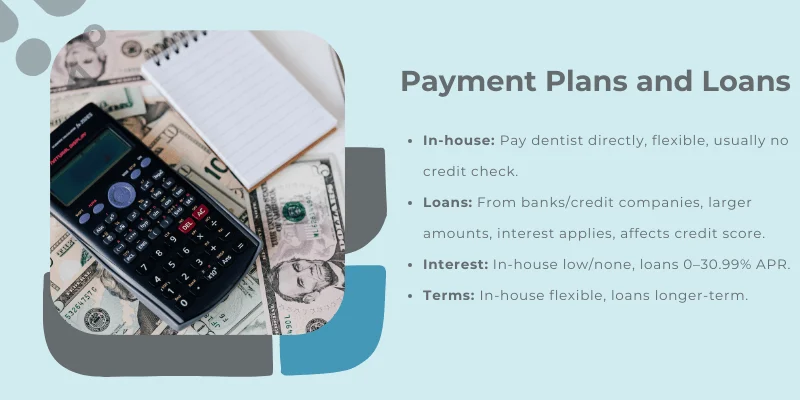

In-House Payment Plans vs. Third-Party Financing

Many dental offices offer in-house payment plans that let you pay the office directly over several months or years. These plans often come with little to no interest if you qualify and can be easier to get approved for than bank loans.

Third-party financing through companies like CareCredit, Cherry, Proceed Finance, and LendingClub gives you more flexible payment options. These third-party lenders partner with dental offices and offer promotional periods with 0% interest if you pay off the balance within a set timeframe, usually 6 to 24 months.

The main difference is who you make payments to and what terms you get. In-house plans keep everything between you and your dentist.

Third-party financing often provides higher borrowing limits and longer repayment terms, but you need to watch out for deferred interest that kicks in if you don’t pay off the full amount during the promotional period.

Dental Loans, Lines of Credit, and Installment Loans

Personal loans from banks or credit unions give you a lump sum upfront to cover your dental implants. You then pay back the loan in fixed monthly payments over a set period, typically 2 to 7 years.

A home equity loan or home equity line of credit uses your home as collateral and usually offers lower interest rates than unsecured personal loans. These work well for full-mouth reconstructions that cost $20,000 or more.

Installment loans specifically for dental work break your total cost into equal monthly payments. Credit unions often provide better rates on personal loans than traditional banks.

Lines of credit work differently by giving you access to funds you can borrow from as needed during your treatment.

Healthcare Credit Cards and Medical Financing

Medical credit cards like CareCredit are designed specifically for healthcare expenses including dental implants. These cards offer promotional financing with 0% APR for 6, 12, 18, or 24 months depending on your purchase amount.

You can use healthcare credit cards at thousands of dental offices nationwide. The application process takes just minutes and you can often get approved the same day as your consultation.

Finance options through medical credit cards work best when you can pay off the balance before the promotional period ends. If you carry a balance past the deadline, you’ll owe deferred interest on the entire original amount at rates often above 25% APR.

Explore flexible dental implant financing options in Schererville and Munster, IN. Visit our Financial Options page to plan your care with confidence:

Using Dental Insurance, HSAs, and FSAs

Many people can reduce their out-of-pocket costs for dental implants by combining different payment methods. Dental insurance typically covers some implant components, while health savings accounts and flexible spending accounts let you pay with pre-tax dollars.

Dental Insurance Coverage and Limitations for Implants

Most dental insurance plans classify implants as a major procedure. Your plan might cover 20-50% of certain implant components after you meet your deductible.

Insurance companies often pay for the crown portion but not the surgical placement of the implant post. Some plans cover bone grafting or extractions that happen before implant surgery.

You should check your policy’s annual maximum because many plans cap benefits at $1,000 to $2,000 per year.

Common Coverage Limitations:

- Waiting periods of 6-12 months for major procedures

- Pre-authorization requirements before treatment

- Missing tooth clauses that exclude teeth lost before coverage started

- Age restrictions for implant coverage

Your insurance might cover a larger portion if you need implants due to an accident rather than tooth decay. Plans sometimes cover dentures at a higher percentage than implants, even though implants last much longer.

Leveraging Health Savings Accounts (HSAs)

A health savings account (HSA) lets you pay for dental implants using pre-tax funds. You must have a high-deductible health plan to qualify for an HSA.

The money you put into your HSA reduces your taxable income. You can use these funds for dental implants without paying taxes on withdrawals.

Your HSA balance rolls over every year, so you can save up for expensive procedures. Health savings accounts allow you to combine HSA benefits with dental insurance coverage and payment plans.

Your insurance might pay for extractions while your HSA covers the implant posts and crowns. You own your HSA even if you change jobs or retire.

Utilizing Flexible Spending Accounts (FSAs)

Flexible spending accounts work similarly to HSAs but have different rules. You can use FSA accounts to pay for qualified dental expenses including implants with pre-tax money.

FSAs require you to use the money within the plan year or lose it. Some employers offer a grace period or let you carry over a small amount.

You need to estimate your dental costs carefully when choosing your FSA contribution amount. Your employer owns the FSA, so you cannot take it with you if you leave your job.

However, you can access the full annual amount right away, even if you have only contributed part of it. This makes FSAs helpful for procedures you plan to complete early in the year.

Medical Expense Reimbursement and Other Employer Benefits

Some employers offer health reimbursement arrangements (HRAs) that can cover dental work. HRAs let your employer contribute pre-tax dollars that you can use for medical and dental expenses.

Your company funds the entire HRA, and you do not contribute your own money. The plan documents determine what expenses qualify for reimbursement.

Some HRAs have specific amounts set aside for dental care.

Additional Employer Benefits:

- Dependent care FSAs for dental work for your children

- Premium-only plans that reduce insurance costs

- Employer-sponsored dental discount plans

You can often combine multiple benefits together. You might use your dental insurance first, then pay remaining costs with your HSA or FSA.

Medical expense reimbursement plans give you more flexibility than traditional insurance for covering implants instead of dentures.

Key Factors Affecting Eligibility and Approval

Your ability to qualify for dental implant financing depends mainly on your credit score, the type of financing you choose, and your income level. Understanding what lenders look for can help you prepare and increase your chances of approval.

Credit Score Requirements and Impact

Your credit score plays a big role in determining whether you’ll get approved for dental implant financing and what terms you’ll receive. Most third-party lenders look at your credit history to decide if you qualify.

A good credit score usually opens the door to better loan terms and lower interest rates. If you have strong credit, you’re more likely to qualify for 0% APR promotional periods through options like CareCredit.

Getting dental implant financing with bad credit is still possible, but your options may be more limited. You might face higher interest rates or shorter repayment terms.

Some lenders still approve applications from people with lower credit scores, though the APR will likely be higher. A higher credit score typically gets you better APR rates and loan terms.

Some lenders offer 0% APR during promotional periods if you have good credit. If your score is lower, you might face higher interest rates or stricter terms.

You might need to consider alternative financing methods or work with providers that specialize in approving applicants with lower credit scores.

Credit Score Requirements and Impact

Your credit score plays a major role in whether you get approved for dental implant financing. Most traditional lenders and third-party financing companies look at your credit history to decide if you qualify.

A good credit score typically means better loan terms and lower interest rates. If you have strong credit, you might qualify for promotional offers like 0% APR during an introductory period.

Poor credit scores can still get approved but usually come with higher interest rates and less favorable terms. Many dental financing options require a good credit score to qualify for the best terms.

Getting approved with bad credit is still possible through certain lenders or in-house payment plans. Some financing companies use soft credit checks during pre-approval, which won’t hurt your credit score.

Hard inquiries happen when you formally apply and can slightly lower your score temporarily.

Approval Process for Different Financing Methods

Third-party financing companies like CareCredit often provide quick approval decisions, sometimes within minutes. These companies usually perform a soft credit check first that won’t hurt your credit score.

In-house dental office payment plans typically have easier approval requirements. Your dentist may not check your credit at all or may be more flexible with requirements.

Personal loans from banks or credit unions take longer to approve. You’ll need to submit income documentation and go through a formal application process.

BNPL (buy now, pay later) options often have the fastest approval times. Many providers decide within minutes using automated systems.

Credit Score Requirements and Impact

Your credit score plays a major role in whether you get approved for dental implant financing. Most dental financing options require a good credit score to qualify for the best terms.

A score above 700 typically qualifies you for better loan terms and lower interest rates. Scores between 600 and 699 may still get approved but often come with higher APR rates.

If your credit score is below 600, you might face challenges getting approved through traditional lenders. Some financing companies offer 0% APR promotional periods if you have good credit.

These deals usually require payment in full within 6 to 24 months. If you miss the deadline, you may owe all the deferred interest at once.

Getting dental implant financing with bad credit is still possible, though your loan terms may include higher interest rates or shorter payment periods. Lower credit scores typically result in higher APR rates and stricter payment terms.

Approval Process for Different Financing Methods

Each financing option has its own approval timeline and requirements. Third-party providers like CareCredit often approve applications within minutes using soft credit inquiries that don’t hurt your credit score.

Personal loans through banks typically take longer and require hard credit checks. In-house dental office plans often have the most flexible approval process.

These plans work directly with your dentist’s office and may not require a credit check at all. Many practices create custom payment arrangements based on your specific situation.

Third-party financing programs can approve applications within minutes using soft credit inquiries. You’ll sign a digital agreement that spells out your repayment terms, interest rate, and monthly payment amount.

Buy now pay later options typically have the fastest approval process with minimal requirements.

Role of Co-Signers and Income

Your income level plays a major role in whether you get approved for dental implant financing. Lenders want to see that you earn enough money each month.

Tips for Affordable Dental Implants and Smart Financing

Finding affordable dental implants requires comparing different financing terms, exploring membership programs that reduce treatment costs, and selecting providers who offer transparent pricing. You can lower your dental implant cost significantly by researching payment structures and choosing the right dental office.

Comparing Payment Plans and Refinancing

You should compare multiple dental financing options before committing to any payment plan. Different providers offer varying interest rates, with some offering 0% APR for qualified patients through programs like CareCredit or Sunbit.

Look at the monthly payment amount, total interest charges, and loan term length. A longer payment plan might seem easier on your budget, but it often costs more in interest over time.

Calculate the total amount you’ll pay after interest to see the real cost.

Key factors to compare:

- APR (annual percentage rate)

- Monthly payment amounts

- Loan term length (12, 24, or 36 months)

- Prepayment penalties

- Late payment fees

If you already have dental implants financing, you might qualify for refinancing at a lower rate. This works best if your credit score has improved since you first financed your treatment.

Contact your lender to ask about refinancing options that could lower your monthly payments or reduce total interest charges.

Dental Savings Plans and Membership Programs

Dental savings plans work differently than insurance. You pay an annual fee (typically $100 to $300) and receive discounts of 10% to 60% on procedures including implant dentistry.

These membership programs can save you thousands on your total treatment cost. Many dental offices offer their own in-house membership plans with specific discounts for major procedures.

Ask your provider if they have a membership option before looking at outside plans.

Benefits of dental savings plans:

- No waiting periods for major procedures

- No annual maximums

- Coverage for pre-existing conditions

- Immediate activation

Some affordable dentist offices combine membership plans with payment plans for dental implants. This approach gives you both the upfront discount and the ability to spread payments over time.

Cost Control Strategies and Discount Programs

Dental schools provide significant savings because students perform procedures under expert supervision. You might pay 30% to 50% less at a dental school clinic compared to private practices.

The trade-off is longer appointment times and multiple visits. Many ways to reduce your dental implant costs include timing your treatment strategically.

Some offices offer promotions during slower months or discounts for paying cash upfront. Ask about package pricing that bundles the implant post, abutment, and crown together.

This often costs less than paying for each component separately. Some providers in California and other states offer specific discount programs for seniors, veterans, or low-income patients.

Money-saving strategies:

- Schedule during promotional periods

- Pay cash for a discount (typically 5% to 10% off)

- Get multiple implants at once for bulk pricing

- Use HSA or FSA funds for tax-free payments

Choosing the Right Dental Office or Provider

The right provider should explain all dental office payment plans clearly before you start treatment. A reputable office will give you a written estimate that includes every cost, from initial consultation to final crown placement.

Look for providers who offer transparent pricing and multiple payment options. Ask if they accept major credit cards, offer in-house financing, or work with third-party lenders.

The best offices partner with several financing companies so you can choose the option with the best terms for your situation. Check whether the dental office includes preliminary procedures like bone grafting or extractions in their quoted price.

Some providers advertise low costs for dental implants in California or other states but add significant charges for necessary preparatory work. Read online reviews about the provider’s billing practices and how they handle insurance claims.

A good dental office will help you maximize any insurance benefits you have and will clearly explain what your plan covers versus what you’ll pay out of pocket.

Contact our team in Schererville or Munster, IN to learn the cost of dental implants and explore flexible financial options designed to fit your budget and treatment needs.

Frequently Asked Questions

People with low credit scores can still get financing, and grants may help reduce costs in certain situations. Payment plans break down the total cost into smaller amounts over time, and many dental offices offer their own financing options.

How can someone with bad credit finance dental implants?

You can still finance dental implants even with bad credit. Many dental offices offer in-house payment plans that don’t require credit checks at all.

Some third-party lenders work with patients who have lower credit scores. You might pay higher interest rates, but you’ll still have access to financing.

Looking into options like CareCredit or LendingClub can help since they consider various credit levels. You could also ask a family member with better credit to co-sign a loan.

This gives you access to better rates and terms. Another option is saving money in a Health Savings Account or Flexible Spending Account to cover part of the cost upfront.

Are there grants available to help cover the costs of dental implants?

Some nonprofit organizations offer dental grants for people who need help paying for implants. These programs usually focus on low-income individuals, veterans, seniors, or people with disabilities.

The Dental Lifeline Network and Cosmetic Dentistry Grants Program are two organizations that might help. You’ll need to apply and show proof of financial need.

Keep in mind that these grants are competitive and not everyone who applies will receive funding. Local dental schools sometimes provide reduced-cost implant procedures.

Students perform the work under close supervision by experienced dentists.

What options do I have for payment plans when considering full mouth dental implants?

Full mouth dental implants cost significantly more than single implants, so payment plans for teeth implants become even more important. Most dental offices understand this and offer extended payment terms for larger procedures.

You can spread payments over several years instead of months. Some plans let you pay over 5 to 7 years for full mouth reconstruction.

This makes monthly payments much more manageable. Third-party financing companies often have special programs for major dental work.

They may offer promotional periods with 0% interest if you pay off the balance within a set time frame. Your dental office can help you compare different options to find what works for your budget.

Can I pay for dental implants in installments, and if so, how does that process work?

Yes, you can pay for dental implants in installments through various financing options. The process starts with discussing payment options during your consultation.

Your dental office will help you apply for financing if you choose a third-party lender. The application takes just a few minutes and you usually get approved the same day.

Once approved, you’ll know your monthly payment amount and interest rate. Most payment plans cover the complete treatment cost, including the implant post, abutment, crown, and any preliminary procedures like bone grafting.

You make monthly payments until the balance is paid off. Some offices let you start treatment before making any payments.

Is in-house financing available for dental implant procedures?

Many dental offices offer in-house financing where you pay the office directly instead of going through a bank or lending company. This option often has simpler approval requirements than traditional loans.

In-house plans typically don’t require credit checks. Your dentist sets the payment terms based on your situation and the cost of treatment.

You might pay little to no interest depending on the office’s policies. These plans work best when you have an established relationship with your dental office.

The office might ask for a down payment, but this isn’t always required. You’ll sign an agreement that outlines your monthly payment amount and due dates.

What are some strategies for affording dental implants without a perfect credit score?

Start by getting quotes from multiple dental offices to find the best price. Prices can vary significantly between providers.

Ask each office about their flexible payment solutions and which ones work with lower credit scores.

Consider using a Health Savings Account or Flexible Spending Account to pay for part of the procedure with pre-tax dollars.

If your dental insurance covers any portion of implants, that amount can be financed separately to reduce what you need to borrow.

Look into dental discount plans as an alternative to insurance. These plans offer reduced rates at participating dentists.

You could also schedule your implants in stages. Paying for one implant at a time instead of all at once may make costs more manageable.

Asking about promotional financing periods helps too. Some lenders offer 0% interest if you pay off the balance within 12 to 24 months.